By Adriel Nisperos

Whatever stage you are in your startup journey, it pays to have a strong understanding of your startup’s foundations. As founders of early-stage startups, having solid foundational knowledge and skills can help you make informed decisions in any aspect of your business.

Here are eight steps to help you create a strong foundation for your startup and improve your organizational capacity. These lessons were taken from the recently concluded IDEA Camp that the IDEA cohort participated in as part of their incubation with us at PhilDev and the Department of Trade and Industry.

[READ: DTI, PhilDev announce 26 tech startups joining ‘IDEA’ and ‘ADVanCE’]

We also took the opportunity to share some tools and guides to get you started.

1. Know your startup’s core

Startups are built to solve a problem. But often, when entrepreneurs are too deep in their product, they forget about why they built the business in the first place. Noreen Bautista, Founder of Panublix, kicked off the camp by discussing the importance of formalizing a startup’s VMG (vision, mission, and goals).

She highlighted that VMGs help in determining the direction of the startup and ensuring that it stays true to its purpose, “It’s a really important question to always keep asking yourself why you are doing this because you need a way to help you endure this whole entrepreneurship journey.”

Your activities and even how you design your product or service will be anchored to your startup’s VMGs. Defining these early on will help you not lose sight of the milestones you want to achieve.

Get started with this tool:

2. Create a sustainable business model

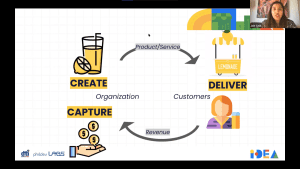

Every successful startup has a sustainable business model. It is one of the criteria that investors and funders look into when investing in a startup. Joie Cruz, Founder and CEO of Limitless Labs, defines a business model as a tool that “describes the rationale of an organization and how it creates, delivers, and captures value.”

Think of it as starting a lemonade stand like Joie illustrated. You create value when you create a refreshing lemonade drink to quench the thirst of your customers. You deliver value when you set up your lemonade stand and begin serving your customers. Finally, you capture value when your customers pay for your drink and support your business.

Think of it as starting a lemonade stand like Joie illustrated. You create value when you create a refreshing lemonade drink to quench the thirst of your customers. You deliver value when you set up your lemonade stand and begin serving your customers. Finally, you capture value when your customers pay for your drink and support your business.

Strategyzer, the company that developed the business model canvas among many other tools, shares seven questions to help entrepreneurs like you assess if your business model is working:

- How much does switching costs prevent your customers from churning?

- How scalable is your business model?

- Does your business model produce recurring revenues?

- Do you earn before you spend?

- How much do you get others to do the work?

- Does your business model provide built-in protection from competition?

- Is your business model based on a game-changing cost structure?

Get started with these tools:

3. Achieve product-market fit

Entrepreneurs and innovators are builders. They love creating game-changing ways to disrupt the status quo. However, building a great product/service is one thing. Ensuring that your product/service addresses a pain point of a lot of people is just as important (some would argue that it’s even more critical).

The journey to achieving product-market fit is different for every startup. But the secret sauce to keeping the journey short is to always talk to your customers and ask for their feedback, so you can build a product that they would pay for.

How would you know if you’re achieving product-market fit? Marc Andreessen, the person who coined the term, describes the situation when your “customers are buying the product just as fast as you can make it.”

For now, you can start your journey by identifying your target customers, talking to them about their pain points, and then creating your customer persona. This step will help you build a minimum viable product that you can iterate over and over until you achieve product-market fit.

Take it from the experience of one of our IDEA cohort startups.

Anne Clarice Ng, Founder and Chief Executive Officer of mobility platform SafeTravelPH, shared that they are currently in the midst of turning their platform into a “full-fledged” startup. They found the sessions on creating a sustainable business model and achieving product-market fit most helpful for their case.

“SafeTravelPH is a product of a research project, so discovering our target market, specifically paying customers, really guided our perspectives on which features to highlight and improve on. The insights we have gathered from the session supports and eases our transition from a knowledge product to an actual startup,” Clarice shared.

Get started with this tool:

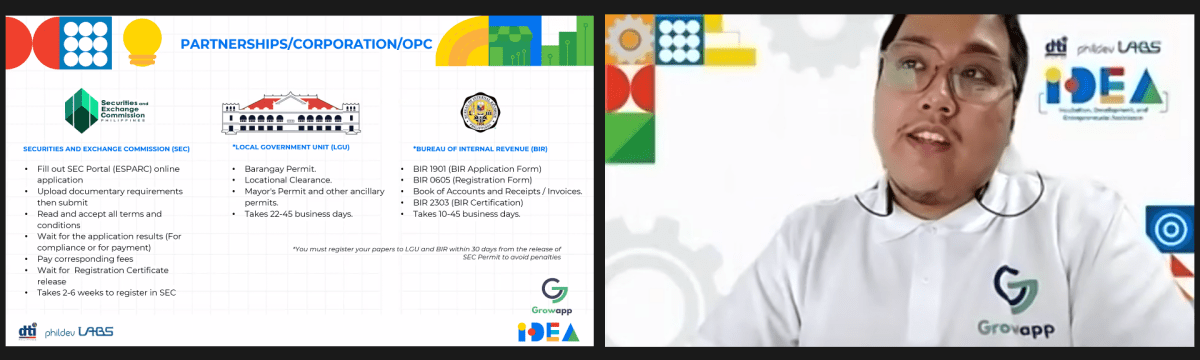

4. Know your legal and documentary must-haves

Government compliance and administrative work are often overlooked in running a startup. Most entrepreneurs focus on their product (which is definitely okay), but having formal documents shouldn’t be an afterthought. When operating here in the Philippines, you need to comply with various government regulations to operate legally and according to standards.

Legal and documentary must-haves depend on your startup’s structure and industry vertical. Is your startup a sole proprietorship, a corporation, or a partnership? Which industry will your startup be operating in? For example, if you’re planning to enter the personal care industry, secure appropriate approvals from the Food and Drug Administration before selling your product in the market.

Giel Nocon, Co-Founder and Chief Operating Officer of Growapp.ph, understands that accomplishing business requirements takes time and resources (as some require fees). For startups and small businesses, this means taking time away from running the business.

However, Giel also emphasized that compliance work is as critical, “Don’t set aside government compliance because this is vital in your business operations. You don’t want to keep focusing on your business models only to end up paying for the penalties for not complying to government regulations.”

Get started with this video guide:

5. Figure out the message of your startup and how to say it

Entrepreneurs talk to a variety of people. From customers to mentors, to investors, to potential partners, even to followers on social media, entrepreneurs essentially have to be master communicators. But many startups struggle in figuring out exactly what to say clearly and effectively.

Trix Rodriguez, Social Media Specialist at Fennel Designs, shared during the camp that creating a communications plan helps a startup (1) introduce themselves to the public, (2) shape the public’s perception about their business, and (3) reach new audiences that could potentially be their customers.

When beginning to craft a communications strategy, Trix invites the entrepreneurs to get to know their audience, “Do you really know who you’re talking to? Even in a normal conversation, it’s hard to communicate if you don’t have an idea who you’re talking to.”

Once you identify your target audience, the next step is to determine what your startup wants to communicate. This key message should be tailored to what your audience needs and wants to know. How your startup will communicate will also depend on the preferences of your target audience whether that be through social media, personal conversations, email exchanges, among many others.

Get started with this tool and guides:

- Download the Customer Persona Canvas

- Digital Storytelling introductory course

- Social Media Management introductory course

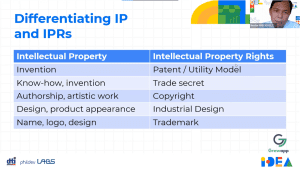

6. Discern when you need to protect your startup

You may have encountered a startup offering a product or service that’s a tad bit too familiar, have you? It’s not a surprise because once a startup becomes successful or even just starts to perform well, others will try to copy them. How can you prevent this from happening?

You may have encountered a startup offering a product or service that’s a tad bit too familiar, have you? It’s not a surprise because once a startup becomes successful or even just starts to perform well, others will try to copy them. How can you prevent this from happening?

During the IDEA Camp, Nestor Precioso, Chief Finance Officer of Growapp.ph, provided the cohort with a refresher course on how they can protect their startups through intellectual property (IP). While some would argue that IP isn’t exactly a concern, Nestor warns that unless entrepreneurs put up their “barriers”, copy-cats can decrease their company’s profits and returns of investments. Moreover, it can also make their competitive advantage disappear.

The World Intellectual Property Organization (WIPO) also cites that startups often undervalue the importance of IP, but they do not immediately realize that some of these concerns might negatively affect their fundraising efforts. WIPO recommends that startups plan for an IP strategy that can protect their business.

Learn more from this guide:

7. Have a strong understanding of your startup’s finances

Managing your startup’s finances is usually done by your accountant, but there are instances where you, as the business leader or founder, will have to make the financial decisions. This is a reminder that Guita Gopalan, General Manager of Vivanti Advantage and Chief Revenue Officer of Ellana Cosmetics, emphasized when she opened the financial management learning session during the IDEA Camp.

Understanding the ins and outs of your startup’s finances is fundamental to every founder. When you know how the money flows inside your business, you can make more sound and informed financial decisions. You will know which areas need more or less financing, and allocate funds to your startup’s priorities.

During Guita’s session, she made sure the cohort was able to develop guiding documents that could help them better understand their startup’s finances. These, according to Guita, will be useful as the startups begin to raise funds.

8. Identify your metrics of success and monitor your performance

All startups aim for success, but success may look different for each of them. What does success look like for your startup? Do you aim to launch your product within the year? Do you want to start earning revenues? Do you want to go overseas and penetrate the global market? It’s easier to run a business when you have set a direction and end goal.

Masaki “Maki” Mitsuhashi, an Innovation and Strategy Consultant, concludes the IDEA Camp highlighting the need for startups to monitor and manage their performance to know whether they are making progress towards their goals. While there are many tools available to measure the performance of a startup, Maki recommends that they consider their team size, reach, budget, and years of existence. These factors will help determine the appropriate tool to measure and monitor their startup’s performance.

If you are a founder of an early-stage startup, Maki suggests using the theory of change and the logic model as starting points. These tools can be applied when conducting due diligence, investment selection, goal-setting, tracking and monitoring progress, aligning incentives, and reporting.

Gillian Santos, Chief Executive Officer of AniTech, an IDEA cohort startup that uses deep technology to address agricultural supply chain problems, shared that they learned a lot from Maki’s session on performance monitoring.

“Working on the logic model was a great matrix to practice on, and it really gave us a chance to think about the short and long term impact we wanted to achieve with AniTech,” Gillian highlighted. She furthered that this tool will be a key document for AniTech as they meet with investors and potential partners.

Get started with this tool:

The entrepreneurship journey, as we always say, is a marathon. If you ask successful entrepreneurs a key lesson they learned throughout their journey, it will most likely boil down to at least one of the eight steps we shared.

For the 20 early-stage startups that participated in the three-day camp, strengthening their foundational knowledge and skills was good preparation to become market-ready.

Caryl and Cris Pizon, Co-Founders of Avodah Philippines, noted that the camp was overall insightful and helpful for them, “We applied almost all we had understood from the camp. We now have a clearer vision, mission, and goals. We had counter checked our business models and realized that we needed to have a performance management system. But most importantly, we learned how to communicate with our audience.”

The Avodah co-founders are also engaging further with Guita Gopalan to seek advice on financial management.

Strengthening your startup’s foundation can enable your business to withstand challenges. Whatever stage your startup is in, revisit your fundamentals. Regularly review and see if you are still heading in the direction you set out for your startup.

With these eight steps we shared with you, we hope you become more equipped to run the entrepreneurial marathon; exit with flying colors.